Welcome to the latest installment of Love & Company’s 2023 blog series on the ever-evolving health of the home resale market. In February 2023, we set the stage with an in-depth analysis of six key performance indicators, exploring how recent trends might influence prospects’ decisions to sell their homes and transition to senior living. In this fifth part to the series, we’ll share some of the shifts we’ve seen since our April, June and September articles, examining the potential impact on the senior living field. Feel free to refer back to our initial blog for baseline details on our ongoing analysis.

Overall Market Analysis

It continues to be a good time for senior living prospects to sell their homes and move to senior living communities, while it also continues to be a bad time for most others to buy homes. High mortgage rates are continuing to limit the supply of homes coming on the market, as potential sellers have lower mortgage rates on their current homes and would have trouble affording to “buy up” (or even downsize) given today’s high rates. Many people are choosing to stay where they are until rates come down.

What this means for senior living prospects is that, with a limited supply of homes to choose from, homes are still selling relatively quickly and at sustained high values.

Mortgage Interest Rate Trends

In our original blog, we noted that mortgage rates declined a bit during the summer of 2022, despite rising federal funds rates, before increasing sharply by late October. After October, mortgage rates fluctuated modestly until about mid-April. However, since April, mortgage rates have steadily increased, reaching their highest rate of 7.56% in mid-October. This increase was likely fueled by the Fed’s increases of the federal funds rate by 0.25% in March, May and July.

Have Higher Mortgage Rates Reduced Home Resale Values?

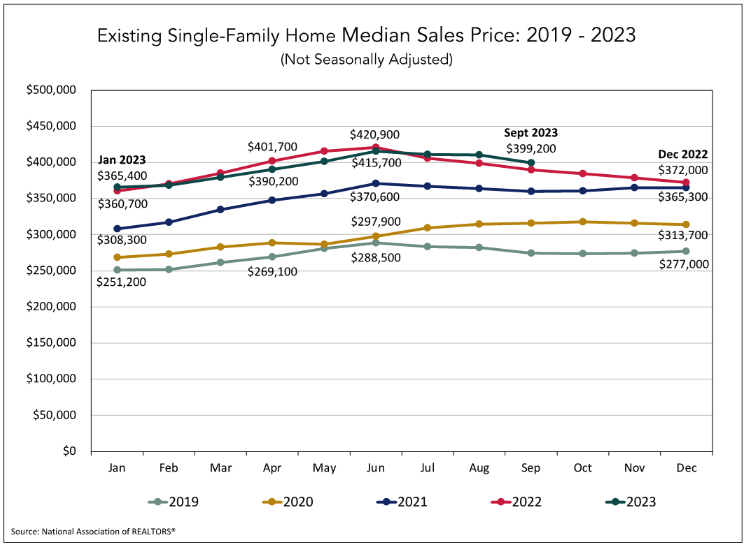

The following graph shows the monthly median home resale value for existing single-family homes from 2019 through September 2023.

The 2023 data continue to show year-over-year median resale values that are holding steady at or higher than 2022 levels, with September data showing a year-over-year increase of about $10,000, or about 2.5%. And while resale prices have declined slightly after peaking in June, this is actually a typical annual pattern based on longer term historical trends, as resale prices typically increase during the spring and early summer peak selling months before declining steadily through the rest of the year. 2020 and 2021 were the exceptions to the rule.

The Pace of Sales

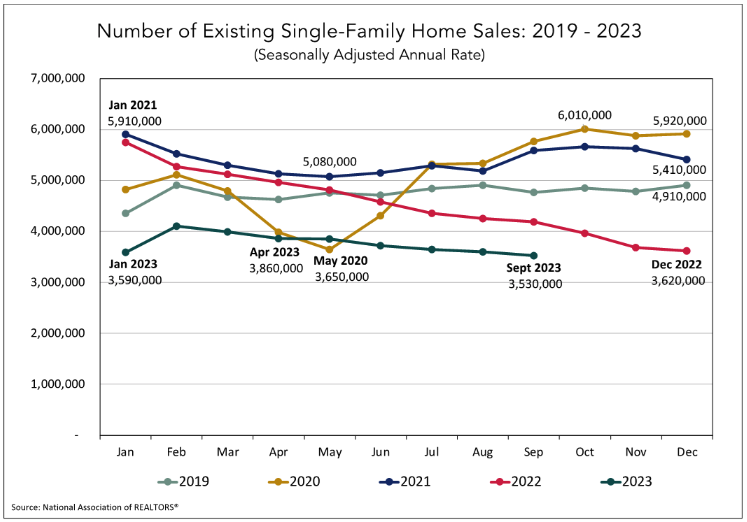

The graph below shows the number of existing home resales by month. The data are shown as an annualized rate of sales based on the number of sales in that month, adjusted for typical seasonality factors.

Not surprisingly, given the high mortgage rates, the number of existing single-family homes that is sold continues to decline each month, though modestly. The year-over-year current sales pace is about 16% lower than 2022 levels.

Supply and Demand and Their Impact on Pricing

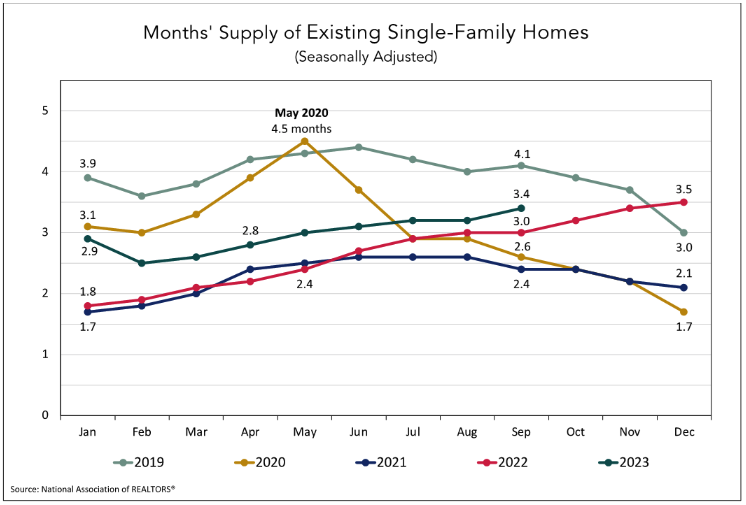

The following graph shows the supply of existing single-family homes for sale (shown as the number of months it would take to sell all the available homes at the current sales pace) for the five-year period from 2019 through 2023.

The supply of homes for sale has continued to increase throughout 2023. This goes hand in hand with the slowing pace of sales noted earlier, as a slower pace means it will take longer to move the current inventory. However, what’s important to note is that the months’ supply is still lower than it was in 2019 (pre-pandemic), when interest rates were in the mid 3%s. What that means is that, even with today’s high interest rates, homes are selling faster than they did when mortgage rates were only about half of today’s rates.

For our senior living prospects, this means that, in today’s market, they can sell their homes relatively quickly and for a healthy price. This is how a low supply of homes works in our prospects’ favor.

What Does 2024 Hold?

It will be interesting to see where the home resale market goes in 2024. We continue to see positive reports about inflation easing, which means the Fed may begin to decrease the federal funds rate in 2024. That could mean lower mortgage rates, which could loosen up the market, bringing a greater supply of homes for sale.

What would lower mortgage rates and an increased supply of homes mean for our prospects? It’s hard to say for sure. On the one hand, the basic laws of economics suggest that a significant increase in supply could make the market more competitive, bringing prices down. On the other hand, lower mortgage rates mean buyers can afford to pay more for homes, which is what helped to push home values so high in the first place. How these market factors wind up playing out will be an important story to follow in 2024.

Love & Company will continue to track these trends into 2024 and report our findings to the senior living field. Stay tuned!